21 Apr Alternative Home Financing Options

The conditions were set for a very competitive housing market. Mortgage rates, housing inventory and unemployment rates were all at record lows. And then COVID-19 changed everything. The federal government implemented a moratorium on foreclosures and asked mortgage servicers to offer forbearance or reduced payments on any mortgage backed by Freddie Mac, Fannie Mae, or the Federal Housing Administration (FHA). But what about subprime or non-QM home financing? Many specialty mortgage lenders have closed and people with less-than-perfect credit have fewer options for home financing.

The market has seen new regulations, mandates, and constant change on the daily. It’s hard for anyone to say what will come next. In such major events, as COVID-19, buyers and sellers are expected to proceed with caution. Consumer sentiment is down due to unemployment and social distancing, yet mortgage rates are holding a steady low.

Mortgage and home applications have seen a rise and fall over the last few weeks. Enough to indicate that buyers are staying optimistic in their long-term plans and that finding a home is a necessary need. Beginning of April, at the peak of the Coronavirus outbreak in the states, home loan applications saw a 12 percent drop; it was the lowest point in over 5 years and down 33 percent annually.

Homeowners saw a break with payment suspension and lenders saw a 3,000 percent spike in requests for suspending or reducing payments. Major Banks, like Chase, Wellsfargo, and specifically Bank of America rolled out deferral for loans, credit cards, and auto loans for up to 90 days. There are certain limitations, and those in good-standing have a better chance of getting the most support. Government-backed loans, those that are through Fannie Mae, Freddie Mac, FHA, or the VA, make up 62% of the total market, according to the Urban Institute.

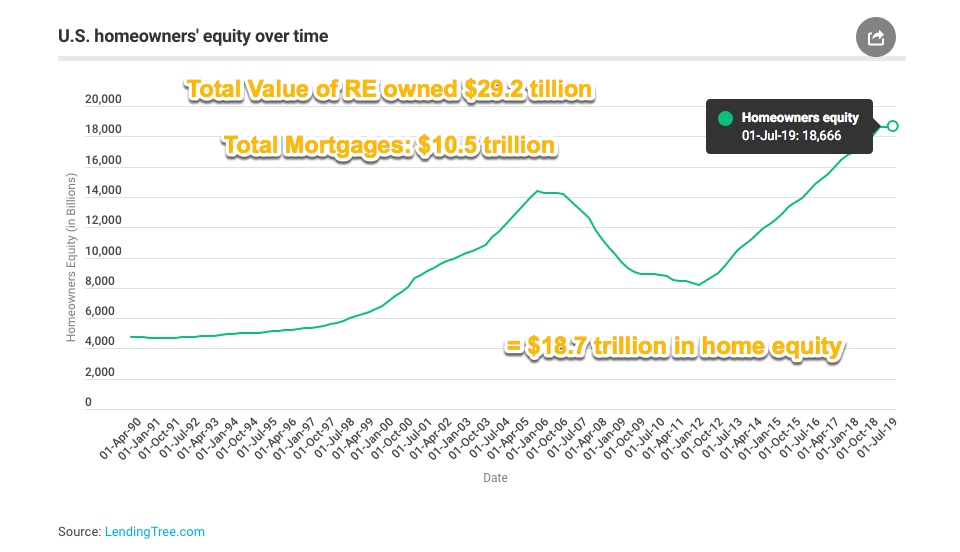

The heads at Caliber Home Loans believes we could surpass the number of delinquencies than during subprime, especially if unemployment continues to rise. The fear of foreclosures is real, but it mostly depends on the duration of the virus persisting and people being away from their jobs. On the positive side, the housing market has been on a good foundation and homeowner equity is at a high, and the majority of lenders are saying that requests are form borrowers in good standing, without any negative marks on their credit and are just in a rut.

CNBC spoke with Sanjiv Das, CEO of Caliber Home Loans on this specific topic:

“I think in 2009 the crisis peaked at 90 days+ delinquencies at 9%, about 9% of the portfolio. I think this time we will get to that peak in about six months. I think it is completely possible that we will go 40-50% on top of that,” Das predicted.

Given the strength of the housing market going into this crisis, the government and bank forbearance programs, and the high value of homes today, experts say those delinquencies are unlikely to yield the high volume of foreclosures seen a decade ago.

Lenders and banks have had to tighten funding and it’s harder to get a loan. So what about those interested in purchasing a home? What are the other options available?

The Veterans Benefits Administration notified veterans that the VA Loan program has specifically worked with lenders and other federal partners. They have lenders helping to remove, reduce, or suspend late fees, or delinquency status for veterans affected by the pandemic. The program is actively seeking how to move forward properly to ease any financial weight. The Administration’s main focus is to keep their veterans safe and at home. The VA loan could potentially help non-members out if they are having issues with their own lender by offering alternative solutions.

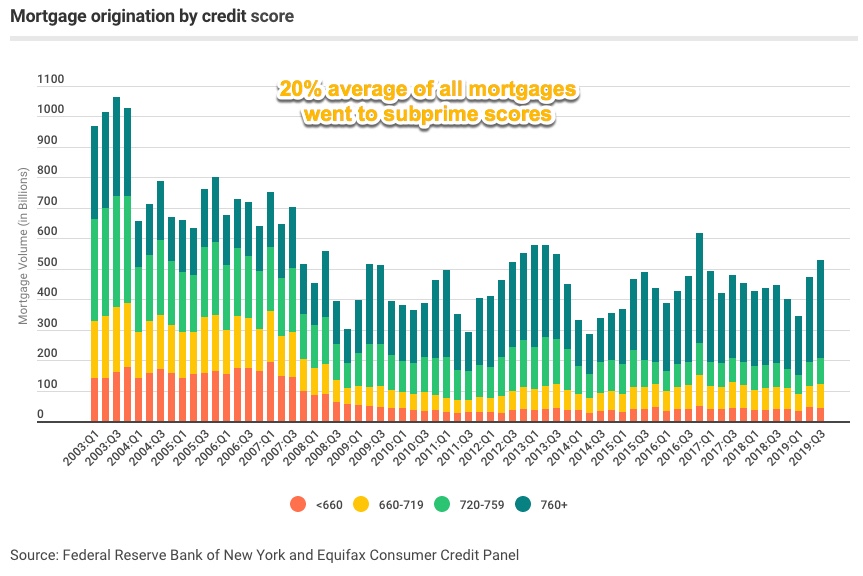

For those holding a less-than-ideal credit score, low income or are having trouble getting approved for any reason – there are options! The Non-Qualified Mortgage or a subprime loan could be a likely solution.

The non-QM loan, also considered a portfolio loan, can help get approval for those who don’t meet the standard requirements for a loan.

How do you know if you qualify for one of these loans? Here are some common situations:

-Low credit score, delinquency or late payment statuses

-Major credit occurrences such as forbearance or bankruptcy

-Unique property type or property issues

-Business owners of Self-Employers who have a unique filing on taxes

-Real Estate Investors

-New to the U.S. looking to invest or purchase real estate

Smaller, local banks or credit unions usually fund these types of loans.

It’s important to understand the difference between this type of loan versus any other traditional loan. Though a non-QM and subprime loan usually has higher rates, or you may need to put more money down upfront, there is a shorter “waiting period.” Getting a portfolio type loan may be a sensible option if the borrower has no other way of obtaining credit or is rejected from other loans.

The purpose of these sorts of loans is that they are short-term to help borrowers build equity. This way, they can avoid renting, work towards a bigger goal, and once they are eligible, they can refinance out of the non-QM or subprime and enter into more traditional financing.

While the market is somewhat on pause from normal activity, active buyers are still on the hunt. They are taking advantage of the low rates and benefit from having less competition. For instance, if rates change even 1 percent lower, that can add an extra $30,000 to the buyer’s budget for a new home. This creates a greater buying power while saving new homeowners tons on monthly payments.

For current homeowners, the biggest question is “Is now the time to refinance?” Mortgage rates hit their lowest back in March and refinance applications skyrocketed almost 80 percent weekly forcing lenders to dismiss new interest. Rates have since increased but are still considered competitive. It’s best to reach out to your loan officer and consider your options. They will guide you and help navigate your goals during this unwavering time.

Every person has been affected by COVID-19 in some way. Each situation is different depending on many factors. Similar to finding a loan, there is an option for every circumstance, and professionals are still working hard to get you the best solution. Make sure to do your research and talk to an expert who can lead you to success.

This article is intended to be accurate, but the information is not guaranteed. Please reach out to us directly if you have any specific real estate or mortgage questions or would like help from a local professional. The article was written by Sparkling Marketing, Inc. with information from resources like MSN, CNBC, Lending Tree, and Forbes.