19 Aug Can Low Rates Help Experts Predict the Rest of 2020?

Consumers and homeowners are taking advantage of some of the lowest rates the housing industry has seen in years. Millennial demand is still high and available inventory is at its tightest. The government continues to find ways to support and stimulate the economy, while millions are still out of work. The housing market continues to be one of the most resilient sectors, despite the unrest. Real estate is expected to hold strong through to 2021 while mortgage rates are anticipated to stay low. These days, we’ve learned anything can happen. And with an upcoming election, economic uncertainty, and a persistent pandemic, professionals inquires if low rates will be able to help sustain a market with such limited inventory?

Since March, when the coronavirus caused drastic change for everyone, mortgage rates and lenders have experienced a restless journey almost on the daily. The Federal Reserve has bought a remarkable amount in mortgage-backed securities and initiated new policies to help stabilize the market and prevent another recession – pushing rates down. It’s indicated that rates will continue to stay low until the economy can see some positive growth. This may not happen until spring 2021 at the earliest.

Mortgage Trends

The historically low rates have been driving buying activity and refinancing. Many lenders and banks were at capacity for weeks due to the overwhelming amount of applications. Purchasing applications reached their highest levels in over 10 years, and the average purchase loan size hit a record high at $365,700 as consumers competed with limited supply and rising home prices. First-time homebuyers accounted for 35 percent of existing-home sales. At one point, refinance activity from homeowners was up 195 basis points from the same time last year. Mortgage application volume finally reached more positive territory at the beginning of July.

As of August 17th, mortgage rates increased for the first time in three weeks to a 3.1 to 3.2 percent average. This is still considered low, but unlike the lows that broke the 3 percent threshold in July for the first time since 1971. The 30-year fixed fell to its lowest at 2.88 percent, and according to the Washington Post, it was the eighth time the popular long-term rate decreased to a ‘new low’ since March.

Summer Real Estate Season 2020

The summer months have proven that consumers don’t want to let a good deal go to waste. Total existing-home sales surged to 20.7 percent, and new home sales surprised experts jumping to 13.8 percent in June. Moving forward in 2020, existing home sales are expected to see a decline of 3 percent, while new home sales may see an increase of 3 percent. The pent up buying demand and lack of supply caused home prices to rise 8.5 percent in July, while national inventory declined 32.6 percent. After a frenzied month, we anticipate for July home sales reports to arrive this month.

Looking Forward in 2020-2021

What do the low rates tell us now as the fall season nears? Experts have been watching to see if recovery will look V-shaped or W-shaped. The majority of predictions see another dip coming before recovery starts to normalize by Spring 2021. This second dip may not be as drastic as before, and experts hope to see it more stabilize but it’s hard to tell with many lingering uncertainties as case numbers rise.

Mortgage rates are expected to hover around low numbers through to 2021. New consumer behaviors have informed forecasts but with many sudden changes in a short amount of time and it being in response to a global crisis, these trends don’t seem likely to last. Will low rates help keep the housing market afloat? Overall, the answer is no. Low rates are not enough to sustain the real estate market alone. The urgent buyers demand from summer is expected to taper off come fall and winter months. There is a predication that cases will jump with schools allowing in-person teaching and more businesses reopening. This could cause another wave of caution for buyers and sellers. But even if the pandemic doesn’t see a resurgence of cases the housing market could see the effect of the pandemic in the slower winter season.

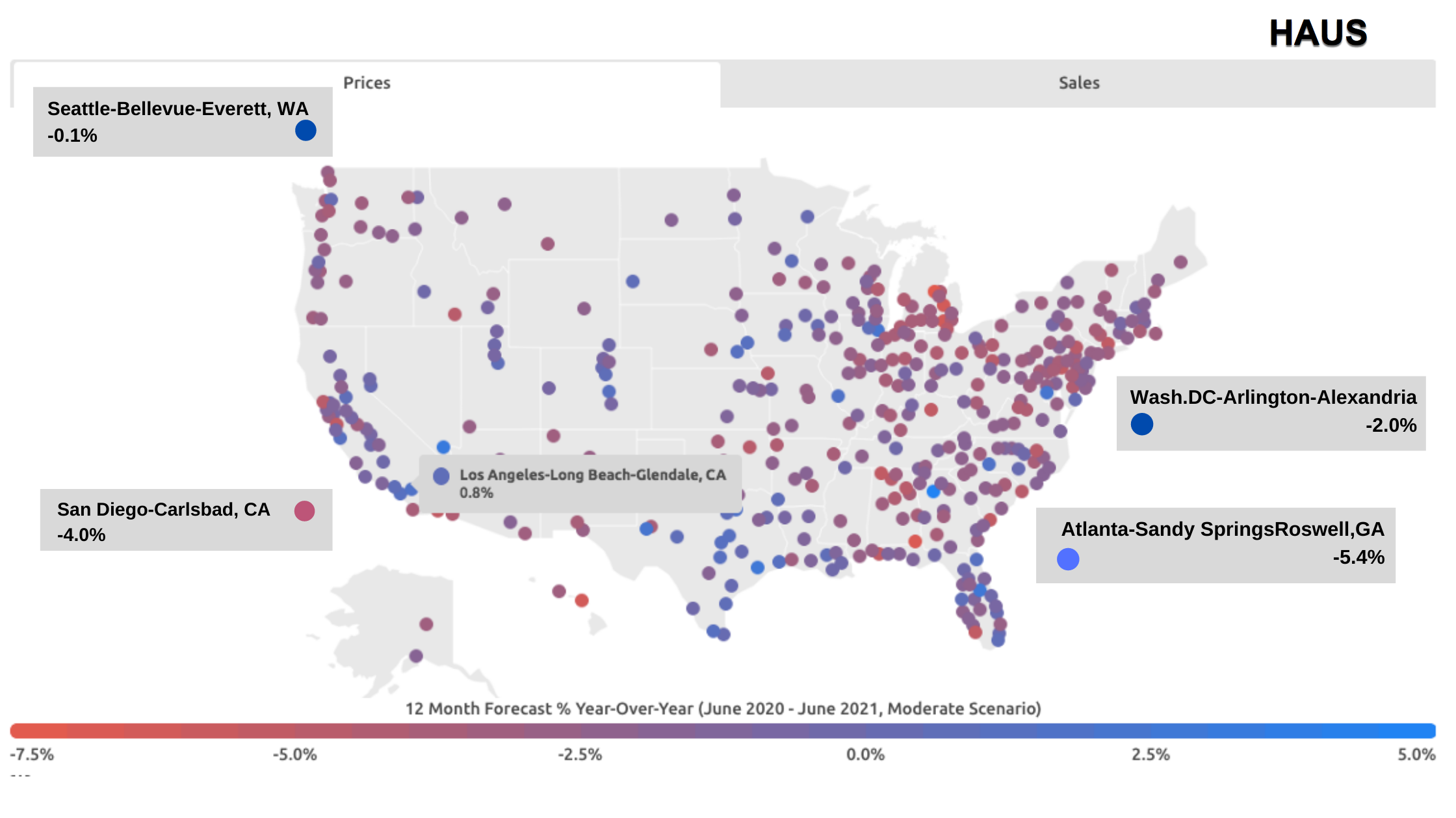

It’s hard to follow any forecast these days. For example, home prices were predicted to drop but as we experienced, they rose due to the competitive nature and tight inventory. The National Association of Realtors (NAR) sees prices appreciating 4 percent before they drop through to fall 2021. Haus also sees home prices falling anywhere from 0.5 to 2.5 percent across the nation starting October of this year through July 2021 as pictured in the image below.

This is all within the hopes that more supply becomes available. Prices will also be determined by progress in a vaccination and safety precautions, and by the forbearance program set for those unemployed.

Foreclosure Activity

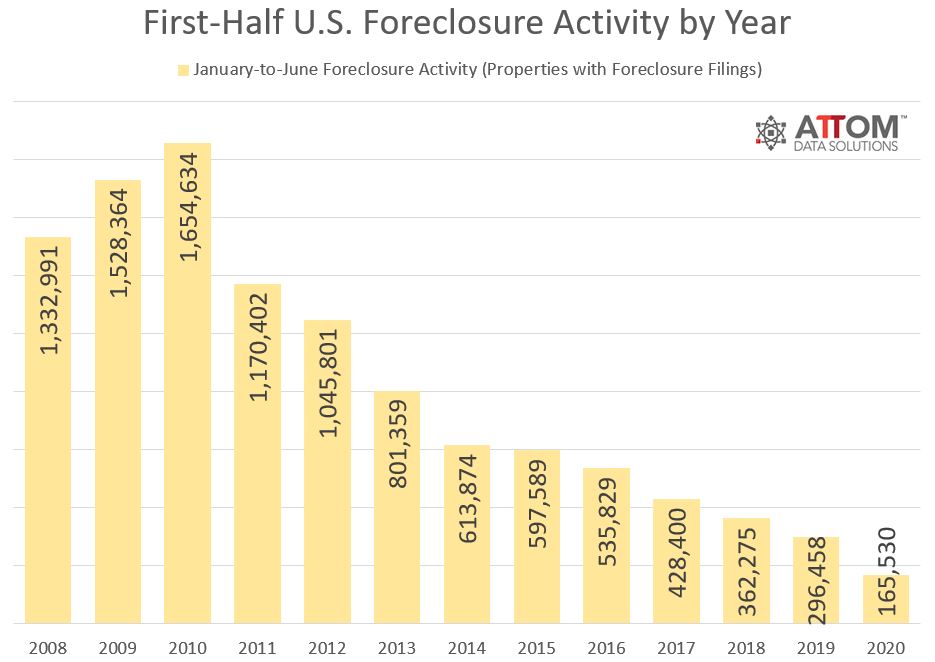

The 2020 U.S. Foreclosure Market Report showed record low foreclosures at 165,530 filings (meaning default notices, scheduled auctions or bank repossessions) in the first half of the year and they continue to decline. This shows a 44 percent decrease, or a total of 37,917 U.S. properties foreclosed, from the first half of 2019. As of July, only 8,892 U.S. properties had a filing, showing a 4 percent decrease from June and 83 percent from a year ago.

With almost 4 million borrowers on the mortgage relief plan, complications with payment relief may arise if the mass unemployment numbers continue. The forbearance program is granted until the summer of 2021. These homeowners are expected to make up for any missed payments. With lower household incomes and still no resolution from the government about extending the CARES Act benefits, foreclosures could make their way into the market. Economist, Ralph McLaughlin mentions: “The [forbearance] policy component is going to be extremely important going forward. We haven’t seen prices fall just yet. However, there are going to be some signs here over the coming months as to whether or not those policies are going to have a lasting impact on housing prices to keep them up, or if there’s potentially going to be a downturn.”

There are a lot of factors to consider when looking ahead. Employment, economic recovery, household income, GDP, and even the 2020 presidential election will all play a role in how quarter-four pans out. For now, it is best to do what you can to stay safe and informed. If you have any questions on how you may be affected, reach out to me directly. I am happy to help guide you to finance success and maximize the best options possible.

This article is intended to be accurate, but the information is not guaranteed. Please reach out to us directly if you have any specific real estate or mortgage questions or would like help from a local professional. The article was written by Sparkling Marketing, Inc. with information from resources like The WashingtonPost, Haus, and NAR.